A Breakdown of What’s Breaking Down in Company Supply Chains

By TRG Advisors on October 27, 2021

Impact and Responses towards Supply Chain Challenges

Q3 was filled with supply chain challenges and capacity bottlenecks. Reporting so far has given us insight into how companies managed those challenges, adapted to cost pressures and met demand. Some did it better than others — and those with proactive management teams, flexible supply chains and pricing power are reporting the best results. An interesting early look at earnings shows that most companies are able to deal with these pressures. So far, of the 29% of S&P 500 market cap that has reported, growth names have reported higher Q3 revenue growth than value (18.2% vs. 12.8%), though value is delivering better margins with stronger EPS growth (41.5% vs. 22.4%) and better Q4 EPS growth expectations (28.6% vs. 12.6%).1

Of course, not all industries are equally exposed to supply chain challenges, or similarly impacted by the inflationary environment. Cyclicals are favorable in environments of high demand and rising prices for those with pricing power. Industrials, have exhibited strong pricing power thus far for their goods and services, as profits expand greater than revenues on a relative basis. Consumer discretionary are also faring well. Companies are leveraging market share to maintain sufficient inventory, have competitive wages to attract labor and have implemented pricing power to meet profit goals. Energy benefits from the supply/demand dynamics that the world is currently facing for oil and natural gas. They are also being helped from the lack of capex over the past several years. And Materials also have the ability to pass along higher inflation in the form of price increases.

Non-cyclicals are dealing with the inflationary pressures in their own ways too. Financials have their own advantages with yield curve exposure, significant deal volume and consumer spending. Health care companies have been sidestepping many of the inflationary pressures and supply chain challenges with their own pricing schedules. Consumer Staples have had a mixed reporting period so far, but all companies in these sectors have been impacted by supply chain challenges and inflationary cost pressures. They have implemented price increases, and it will be worth watching the potential for demand destruction. Information Technology and Communication Services have been immune to the inflation issues and also have strong FCF generation to fund their growth.

Geographic Exposure

Companies that rely on goods coming from facilities around the globe are exposed to the constraints in the shipping industry and an uneven recovery from the pandemic. This has been a significant logistical challenge that starts with COVID-related shutdowns at manufacturing facilities in Asia, followed by Asian port closures due to COVID outbreaks, shipping capacity constraints due to widespread industry re-opening demand and then domestic port bottlenecks that leave cargo sitting idle for up to a month at a time before it is moved inland. Overall, ocean freight costs have more than doubled and nearly 500,000 shipping containers are currently stuck off the coast of Southern California.2

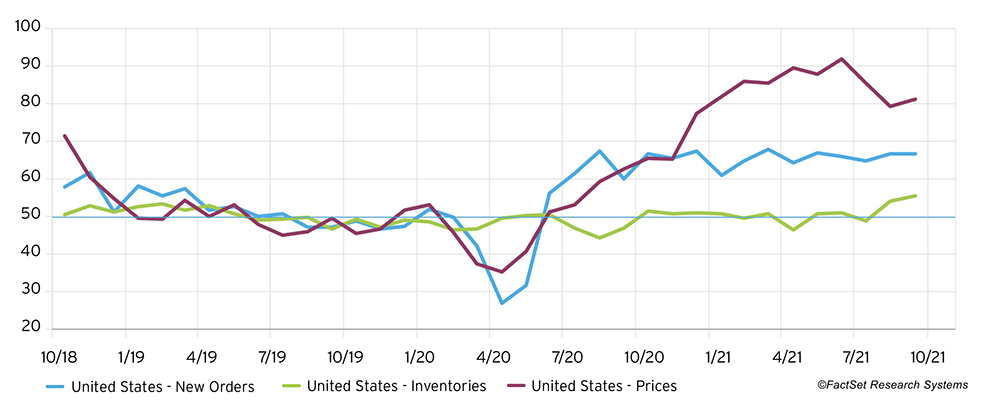

Once inland, trucking capacity constraints have made moving goods difficult, but relative to shipping challenges, the domestic freight capabilities have been more efficient. Order backlog has expanded for fifteen consecutive months, and inventories have not been able to meet the same expansion rate as new orders (levels above 50 indicate m/m expansion).3

Working to meet high demand, some companies have been able to more effectively manage these obstacles by dual sourcing and/or chartering their own ships to partly avoid capacity constraints, though still paying higher costs. One of the positives is that the supply constraints and port issues will eventually get resolved. The timing is a big question, but the companies we talk to have said second half of 2022. In the meantime, this very well might extend the cycle for many industries, which is good news.

Labor Shortages Promote Capacity Constraints

Labor shortages have been widespread, especially in the service sectors — everywhere from ports to restaurants. A shortage of labor is impacting the ability for companies to meet demand, resulting in higher overtime costs. Some companies that hired at the beginning of the year, ahead of current labor market challenges, are in a better position when it comes to productivity and capacity to meet demand. We’re seeing many cases of increased order demand but production unable to keep up, due to longer lead times and insufficient labor. But again, it’s all about pricing power, and those that have it have seen stronger operating profits and earnings.

Initial claims have hit a post-pandemic low, which means companies are doing a better job at retaining labor — likely with better incentives — and the unemployment rate is reaching new lows every month (now 4.8%). Job openings are still roughly 3,000 openings above pre-pandemic levels, and labor participation is being closely watched — an important indicator if we’re going to get back to pre-pandemic labor numbers, especially in sectors like restaurants and hospitality. The labor force is now roughly 3 million less than it was pre-pandemic, and the number of employed is roughly 5 million less.4

1 Source: Credit Suisse

2 Source: Business Insider

3 Source: FactSet

4 Source: U.S. Bureau of Labor Statistics